Key Takeaways

- CD interest earned in 2024 counts as taxable income and can push you into a higher Medicare IRMAA bracket in 2026.

- Single filers earning above $106,000 in modified adjusted gross income will pay surcharges of $70.90 to $419.30 per month on top of the standard Part B premium.

- You can file an IRMAA appeal (Form SSA-44) if you've experienced a qualifying life-changing event that reduced your income.

- Strategic income planning — including tax-loss harvesting, Roth conversions, and staggering CD maturities — can help you stay below IRMAA thresholds.

The CD Windfall That Could Cost You More Than You Think

In 2024, millions of Americans — many of them retirees and pre-retirees — locked in certificates of deposit paying 5% or more. It felt like a no-brainer. After years of near-zero interest rates, banks were suddenly offering returns that hadn’t been available since the early 2000s. If you moved $200,000 into a 12-month CD at 5.1%, you pocketed roughly $10,200 in interest. Congratulations — and I mean that sincerely.

But here’s what I’ve been warning my clients about since late 2023: that $10,200 is fully taxable ordinary income, and it doesn’t just affect your April tax bill. It can quietly raise your 2026 Medicare premiums through a mechanism most people have never heard of called IRMAA — the Income-Related Monthly Adjustment Amount. In my 18 years of financial planning practice, I’ve watched this catch more retirees off guard than almost any other provision in the tax code.

Let me walk you through exactly how this works, what the dollar impact looks like, and — most importantly — what you can do right now to manage it.

What Is IRMAA and Why Does It Matter?

IRMAA stands for Income-Related Monthly Adjustment Amount. It’s a surcharge that higher-income Medicare beneficiaries pay on top of the standard Part B (medical insurance) and Part D (prescription drug) premiums. The Social Security Administration determines your IRMAA based on your modified adjusted gross income (MAGI) from your tax return two years prior.

This two-year lookback is the critical detail. Your 2026 Medicare premiums are based on your 2024 tax return — the same year you collected that generous CD interest. So income decisions you made 18 to 24 months ago are about to show up on your Medicare bill.

How MAGI Is Calculated for IRMAA

Your MAGI for IRMAA purposes includes your adjusted gross income (AGI) plus any tax-exempt interest income (like municipal bond interest). That means virtually every dollar of income shows up:

- CD and savings account interest

- Traditional IRA and 401(k) distributions

- Social Security benefits (the taxable portion)

- Capital gains from stock or real estate sales

- Roth conversion amounts

- Rental income, pension income, and annuity payouts

- Tax-exempt municipal bond interest (yes, even this counts for IRMAA)

What I see most often is retirees who carefully manage their tax bracket but forget that IRMAA uses a broader income measure. A Roth conversion combined with CD interest combined with a one-time capital gain can stack up fast.

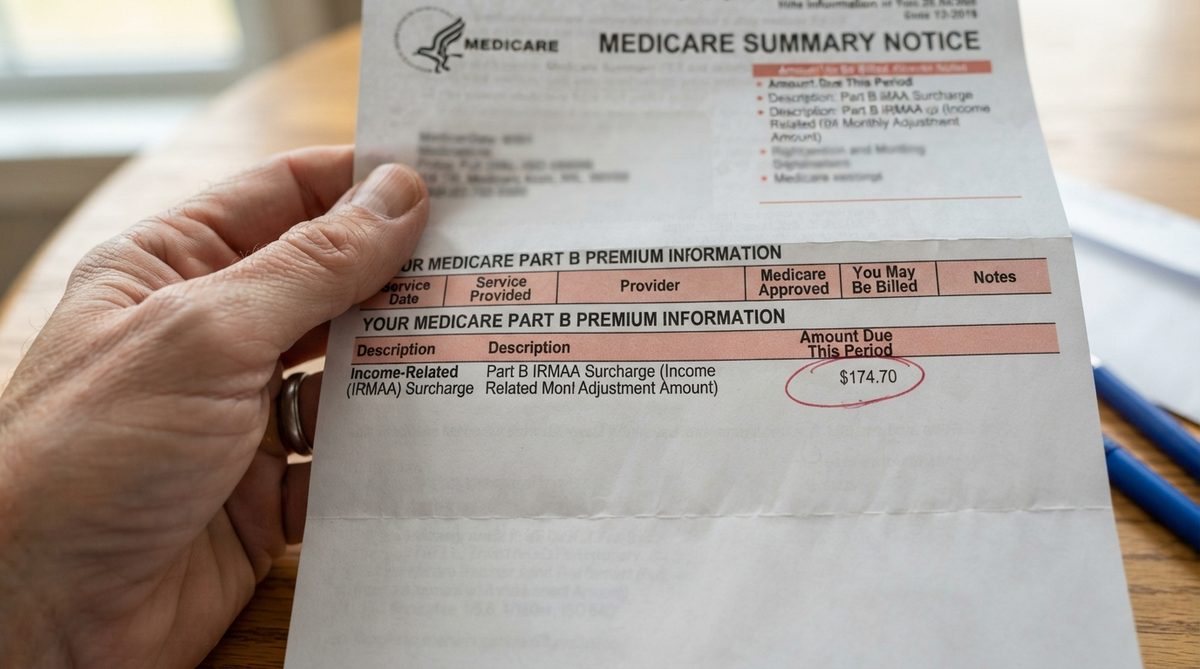

The 2026 IRMAA Brackets: Know Your Numbers

The official 2026 IRMAA thresholds won’t be finalized by CMS until late 2025, but based on current inflation adjustments and the 2025 brackets, here’s what we can reasonably project. The standard Part B premium for 2025 is $185.00 per month. Below is a breakdown of the surcharge tiers using 2025 figures as a close proxy for 2026:

| MAGI (Single Filer) | MAGI (Married Filing Jointly) | Monthly Part B Premium | Monthly IRMAA Surcharge |

|---|---|---|---|

| $106,000 or less | $212,000 or less | $185.00 | $0.00 |

| $106,001 – $133,000 | $212,001 – $266,000 | $259.00 | $74.00 |

| $133,001 – $167,000 | $266,001 – $334,000 | $370.00 | $185.00 |

| $167,001 – $200,000 | $334,001 – $400,000 | $480.90 | $295.90 |

| $200,001 – $500,000 | $400,001 – $750,000 | $591.90 | $406.90 |

| Above $500,000 | Above $750,000 | $628.90 | $443.90 |

Notice that the first threshold for a single filer is $106,000. For a married couple filing jointly, it’s $212,000. These aren’t high-roller numbers. A retired couple with two Social Security checks, a modest pension, and $250,000 in CDs earning 5% can land in the first surcharge tier without even trying.

And here’s what stings: IRMAA applies to both spouses. If you’re married and both on Medicare, that $74 monthly surcharge becomes $148 per month — or $1,776 per year — just for Part B. Add in Part D surcharges, and the total can exceed $2,400 annually.

A Real-World Example: How $10,000 in CD Interest Costs You $1,800

Let me show you a scenario I’ve worked through with several clients this year.

Joan is a 68-year-old single retiree in Phoenix. Her 2024 income looked like this:

- Social Security benefits: $28,800 (85% taxable = $24,480)

- Traditional IRA RMD: $62,000

- Pension: $12,000

- Municipal bond interest: $3,500

- CD interest (two 5% CDs): $10,200

Her MAGI for IRMAA purposes: approximately $112,180. Without the CD interest, she’d have been at $101,980 — safely below the $106,000 threshold. That $10,200 in CD interest pushed her into the first IRMAA bracket, adding $74 per month to her Part B premium and roughly $13.70 per month to her Part D premium. That’s an extra $1,052 per year in Medicare costs — effectively wiping out 10% of her CD earnings.

When you factor in federal income tax at the 22% bracket ($2,244) and state income tax, Joan’s $10,200 in CD interest netted her closer to $6,500 after taxes and the IRMAA hit. Still positive — but a far cry from the headline 5% yield.

Why This Problem Is Bigger Than Most People Realize

According to Investopedia, Americans poured over $3 trillion into CDs and high-yield savings accounts during 2023 and 2024 as rates spiked. A significant share of that money belongs to people over 60 who were — reasonably — looking for safe, guaranteed returns.

The trouble is that CDs generate the least tax-efficient form of income: ordinary interest, taxed at your highest marginal rate and fully counted toward IRMAA. Compare that to qualified dividends or long-term capital gains, which are taxed at preferential rates (0%, 15%, or 20%) and, while still counted in MAGI, may actually produce a lower total tax burden per dollar of return.

I often tell my clients that the yield on a CD is only half the story. The other half is where that income lands on your tax return — and what downstream costs it triggers. For a deeper look at how inflation and income interact with retirement security, I’d recommend reading How to Protect Retirement Savings From Inflation in 2026.

Steps You Can Take Right Now

Review Your 2024 Tax Return Before IRMAA Notices Arrive

Social Security typically mails IRMAA determination letters (Form SSA-4041) in late fall for the following year. If your 2024 MAGI crossed a threshold, you’ll hear about it before January 2026. Pull up your 2024 return now and check Line 11 (AGI) plus any tax-exempt interest from Schedule B. That sum is your IRMAA MAGI.

File an IRMAA Appeal If You Qualify

The SSA allows you to appeal your IRMAA determination using Form SSA-44 if you’ve experienced a “life-changing event” that reduced your income. Qualifying events include:

- Marriage, divorce, or death of a spouse

- Work stoppage or work reduction

- Loss of income-producing property (disaster, etc.)

- Loss of pension income

- Employer settlement payment cessation

Unfortunately, “I didn’t know my CDs would raise my premiums” is not a qualifying event. But if your 2025 income is substantially lower than 2024 due to CD maturities not being renewed, retirement, or any listed event, you may be able to use more recent income figures instead.

Stagger CD Maturities Across Tax Years

If you’re still holding CDs or planning to reinvest, consider spreading maturities so that interest income doesn’t spike in a single tax year. A CD ladder with 6-month, 12-month, 18-month, and 24-month terms distributes income more evenly and can help you stay below an IRMAA threshold.

Consider Tax-Advantaged Alternatives

Depending on your situation, some alternatives to taxable CDs may reduce IRMAA exposure:

- Treasury I Bonds: Interest can be deferred until redemption, giving you control over when the income appears on your return.

- Municipal bonds or muni bond funds: Interest is federally tax-free (though it still counts toward IRMAA MAGI — be careful).

- Roth IRA holdings: Qualified Roth distributions don’t count toward MAGI at all. If you’re under 73, converting a portion of traditional IRA assets to Roth now — even though the conversion itself is taxable — can reduce future IRMAA exposure.

- Health Savings Accounts (HSAs): If you’re still eligible (under 65 and on a high-deductible plan), HSA contributions reduce AGI.

Time Roth Conversions Strategically

Roth conversions are one of the most powerful long-term tools for managing IRMAA, but they require careful timing. Converting too much in a single year can itself push you into a higher IRMAA tier. I typically recommend what I call “bracket-filling” conversions: converting just enough each year to fill your current tax bracket without crossing the next IRMAA threshold.

For example, if you’re a single filer with a MAGI of $95,000, you have about $11,000 of room before hitting the $106,000 IRMAA threshold. A Roth conversion of $10,000 uses that space efficiently — you pay tax now but shield that money from future RMDs and future IRMAA calculations.

Coordinate With Your Overall Financial Concerns

IRMAA is just one piece of the retirement income puzzle. If you’re navigating multiple financial stressors — from healthcare costs to inflation to market volatility — you’re not alone. A recent survey found that healthcare expenses and outliving savings rank among the 5 biggest financial concerns for retirees in 2026. Addressing IRMAA is part of a broader strategy that should include tax planning, withdrawal sequencing, and estate considerations.

The Bigger Picture: Income Planning Is Healthcare Planning

What this CD-to-IRMAA connection really illustrates is something I’ve been emphasizing for years: in retirement, your income strategy is your healthcare cost strategy. Every dollar of reportable income can affect what you pay for Medicare, how much of your Social Security is taxable, and whether you qualify for various credits or subsidies.

Traditional financial advice treats investment returns, taxes, and healthcare costs as separate buckets. But for retirees, these three streams converge on your tax return. A $10,000 CD that earns 5% might cost you $1,000 in IRMAA surcharges, $2,200 in federal taxes, and $400 in state taxes — leaving you with a real after-cost return closer to 3.2%. That’s still better than nothing, but it changes the calculus, especially if a Treasury I Bond or Roth-held investment could have delivered a similar return with none of those side effects.

Don’t Panic — But Do Plan

I want to be clear: if you bought CDs in 2024, you didn’t make a mistake. You earned a solid, safe return in a volatile market environment. The issue isn’t the CD — it’s the lack of awareness about how that income ripples through the retirement planning ecosystem.

The good news is that IRMAA is reassessed every year. If your 2025 income drops back below the threshold (because those CDs matured and you didn’t reinvest at the same scale, or because you shifted to more tax-efficient holdings), your 2027 premiums will reflect that lower income. This isn’t a permanent trap — it’s a one-year hit that you can plan around going forward.

If you’re feeling overwhelmed by the financial complexities of retirement, remember that staying engaged — whether through managing your finances, pursuing hobbies, or simply staying curious — is one of the most powerful things you can do for both your financial and overall well-being.

Your Action Checklist for the Next 60 Days

- Pull your 2024 tax return and calculate your MAGI (AGI + tax-exempt interest).

- Compare your MAGI to the IRMAA threshold table above.

- If you’re over a threshold, estimate the annual cost of the surcharge for both Part B and Part D.

- Determine whether you qualify for an IRMAA appeal via Form SSA-44.

- Meet with a CFP® or tax advisor to map out a 2025–2026 income strategy that avoids repeating the spike.

- Evaluate whether CD reinvestment, Roth conversions, or I Bond purchases better serve your after-tax, after-IRMAA goals.

The retirees who come out ahead aren’t the ones who chase the highest yield — they’re the ones who understand what they keep after taxes, premiums, and surcharges. That’s the number that funds your retirement. And it’s the number worth planning around.

About Margaret Chen, CFP®, MBA Finance

Margaret Chen is a Certified Financial Planner™ (CFP®) with more than 18 years of experience guiding American seniors through retirement planning, Social Security optimization, and Medicare decisions. She holds an MBA in Finance and has dedicated her career to helping retirees protect their savings, maximize their benefits, and avoid the most common financial mistakes that derail retirement. At Daily Trends Now, Margaret writes practical, fact-checked guides that translate complex financial topics into clear action steps for older Americans.