The Phone Call That Changed How I Think About Retirement Advice

Last March, I got a call from a client I’ll call David. He’s 71, lives outside of Fort Worth, Texas, and retired in 2019 with what he and his wife Linda considered a comfortable $640,000 in savings. They had a plan. They’d done the math. They’d even hired a financial advisor a decade earlier to help them build a withdrawal strategy.

“Robert,” he said, his voice tight, “we’re burning through our savings almost twice as fast as we expected. We haven’t changed how we live. We don’t take vacations. But our grocery bill is up $280 a month, our homeowner’s insurance tripled, and Linda’s medications cost more every quarter. What the hell happened?”

What happened is inflation — the quiet, relentless kind that doesn’t make front-page headlines anymore but is systematically dismantling the retirement plans of millions of Americans. In my 20 years as a CPA and Enrolled Agent, I’ve never fielded more panicked calls from retirees than I have in the past 18 months. David and Linda aren’t outliers. They’re the norm.

The Numbers Don’t Lie: Inflation Is Draining Retirement Savings at an Alarming Pace

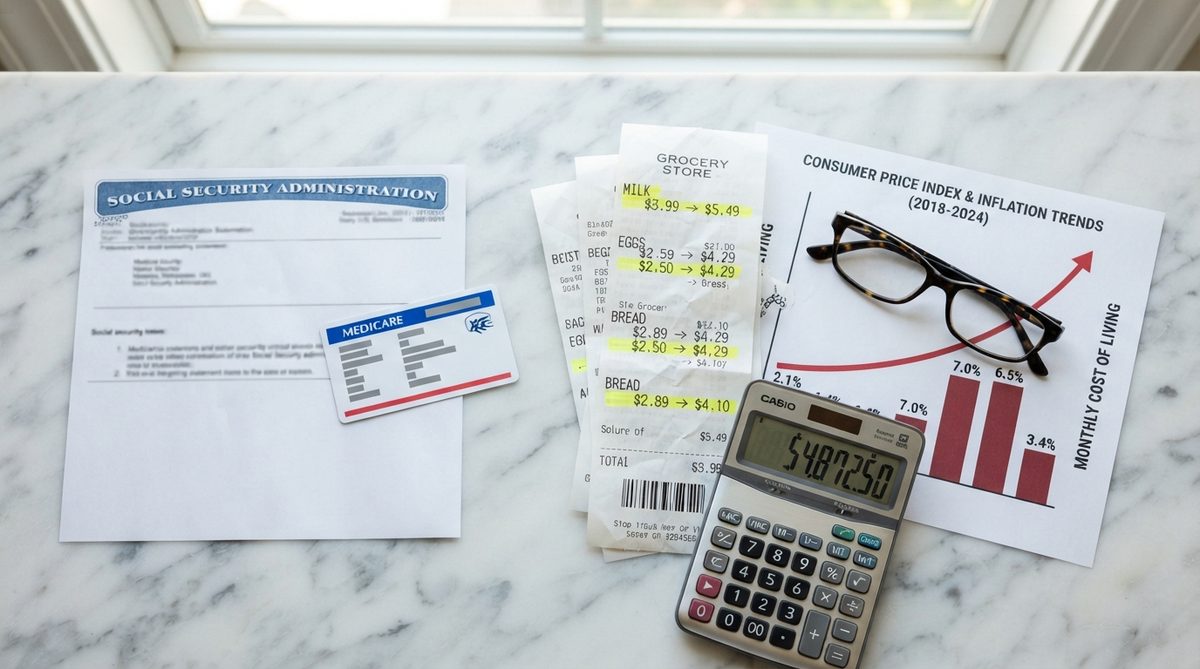

A recent survey from the Employee Benefit Research Institute found that 45% of retirees are depleting their savings faster than they originally projected. Among those aged 65 to 74, the number climbs to nearly 52%. The culprit isn’t reckless spending — it’s the compounding effect of prices that rose 20% or more across essential categories between 2021 and 2025, while Social Security cost-of-living adjustments (COLAs) totaled only about 16% over the same stretch.

That gap — roughly four percentage points of cumulative purchasing power lost — translates to real dollars vanishing from real accounts. For someone withdrawing $3,500 a month from a portfolio, that gap means an extra $1,680 a year pulled from savings just to maintain the same standard of living. Over a decade, that’s nearly $17,000 in additional drawdowns that were never part of the plan.

“Inflation doesn’t have to spike to 9% to be dangerous. A sustained 3.5% inflation rate will cut the purchasing power of a fixed-income retiree’s savings in half within 20 years. That’s not a hypothetical — that’s basic math, and it’s the reality millions of seniors are living right now.”

As I’ve written before, retirees are depleting savings faster than expected, and the trend is accelerating into 2026. The question isn’t whether this is happening. The question is what you do about it.

Where the Money Is Actually Going: A Category-by-Category Breakdown

When I sit down with clients like David and Linda, the first thing I do is dissect their spending into categories. The results almost always surprise them. Here’s what I’m seeing across my practice in 2026:

Food and Groceries

According to the Bureau of Labor Statistics, food-at-home prices are still 2.8% higher year-over-year as of April 2026. That might sound modest, but it’s stacked on top of the 25% cumulative increase since 2020. A retiree couple spending $650 a month on groceries in 2020 is now spending roughly $815 for the same cart. That’s $1,980 more per year — money that was supposed to stay invested.

Healthcare and Medicare Costs

This is the category I see draining savings most aggressively. The standard Medicare Part B premium rose to $185 per month in 2026, up from $174.70 in 2025. But the real danger lurks in Medicare’s Income-Related Monthly Adjustment Amount (IRMAA), which can push premiums dramatically higher for retirees who inadvertently cross income thresholds — often because of Required Minimum Distributions (RMDs) or one-time capital gains from selling a home.

I’ve detailed the mechanics of this in a separate piece on how retirees can avoid higher IRMAA brackets in 2026, and I’d encourage anyone paying more than the standard Part B premium to read it carefully.

Housing and Insurance

Even retirees who own their homes outright aren’t immune. Property taxes in Texas rose an average of 8.3% in 2025, and homeowner’s insurance premiums in the Gulf Coast states and Florida have surged 40–60% since 2022 due to climate-related risk reassessments. David’s insurance went from $1,900 a year to $5,400 — an increase that alone consumed an extra $3,500 annually from savings he can’t replace.

Energy and Utilities

Electricity costs are up 4.1% nationally in 2026, but in states like Texas and Arkansas, the increases are steeper. Seniors living in older, less efficient homes — and many are, since most homes aren’t set up for aging in place — face utility bills that can run $100 to $200 higher per month during summer peaks.

Why the 4% Rule Is Failing This Generation of Retirees

For decades, the financial planning industry leaned on the “4% rule” — the idea that you could safely withdraw 4% of your portfolio annually, adjusted for inflation, and not run out of money over a 30-year retirement. It was elegant. It was simple. And for many of my clients, it’s proving dangerously inadequate.

The rule was developed by financial planner William Bengen in 1994 using historical data that assumed a relatively moderate inflation environment and a balanced stock-bond portfolio. What it didn’t account for was a period where inflation ran hot for years while bond yields remained historically low, followed by a rapid rate increase that crushed bond values.

What I see most often is retirees who entered retirement between 2018 and 2022 following this rule, only to discover that the real inflation rate on goods and services they actually use — food, healthcare, insurance, and utilities — ran 2 to 3 percentage points higher than the Consumer Price Index suggested. The CPI includes categories like electronics and apparel that tend to deflate, dragging down the headline number. But a 72-year-old isn’t buying flat-screen TVs every month. She’s buying prescriptions and eggs.

I now tell most of my clients to plan around a 3.2% to 3.5% initial withdrawal rate if they retire before 67, and to build in a dynamic adjustment mechanism — reducing withdrawals by 5–10% in years when markets decline more than 15%.

A Real Plan to Fight Back: Seven Steps I Walk My Clients Through

Feeling anxious after reading all of this? Good — that means you’re paying attention. But anxiety without action is just suffering. Here’s the specific playbook I use with clients who are watching inflation drain their retirement savings. These aren’t abstract tips. They’re the exact steps I walked David and Linda through.

- Run a “real spending” audit for the past 12 months. Pull every bank and credit card statement. Categorize spending into essentials (housing, food, healthcare, utilities, insurance) and discretionary (dining out, travel, subscriptions, gifts). Most of my clients discover $200–$400 in monthly subscriptions, memberships, or recurring charges they’ve forgotten about. David found $340 a month in charges he didn’t recognize, including a $79/month identity protection plan he’d accidentally signed up for twice.

- Recalculate your withdrawal rate using today’s portfolio value — not the value when you retired. If your $640,000 portfolio is now worth $540,000 and you’re still withdrawing $2,100 a month, your effective withdrawal rate isn’t 4% — it’s 4.7%. That difference can shave five or more years off your portfolio’s lifespan. Use a free calculator at SSA.gov to check your current Social Security benefit and factor that into your total income picture.

- Review your Medicare coverage during every Open Enrollment period — without exception. I see retirees staying on the same Part D or Medicare Advantage plan for years out of inertia. Drug formularies change annually. A medication that was Tier 1 last year might be Tier 3 this year, costing you hundreds more. Spend two hours every October comparing plans at Medicare.gov. It’s the highest-paid two hours of work you’ll do all year.

- Manage your Adjusted Gross Income (AGI) to stay below IRMAA thresholds. For 2026, the first IRMAA surcharge kicks in for individuals with modified AGI above $106,000 and couples above $212,000. A single Roth conversion done carelessly can push you into a bracket that adds $840 or more per year to your Medicare premiums — for each spouse. Timing Roth conversions, spreading capital gains across tax years, and using Qualified Charitable Distributions (QCDs) from IRAs after age 70½ are all tools I use with clients to stay below these lines.

- Rebalance your portfolio toward inflation-protected assets. Treasury Inflation-Protected Securities (TIPS), I-Bonds (capped at $10,000 per person per year through TreasuryDirect.gov), short-duration bond funds, and dividend-paying equities with a history of increasing payouts are all worth discussing with your advisor. I’m not suggesting you overhaul your entire portfolio, but having 15–25% of fixed-income holdings in inflation-linked instruments makes a material difference over a decade.

- Delay Social Security if you’re between 62 and 70 and can afford to. Every year you delay past your full retirement age increases your benefit by 8%. That’s guaranteed, inflation-adjusted income for life. For a retiree whose full retirement age benefit is $2,400 a month, waiting from 67 to 70 increases the monthly check to $2,976 — an extra $6,912 per year. Over a 20-year retirement, that decision is worth over $138,000 in additional income. I’ve seen this single choice transform a client’s financial trajectory more than any investment decision.

- Explore part-time income or monetize a skill — even modestly. I know this isn’t what anyone wants to hear, but earning $800 to $1,200 a month through consulting, tutoring, bookkeeping, or freelance work can reduce portfolio withdrawals by 25–35%. That extended runway can mean the difference between financial stability at 85 and running out of money at 80. And contrary to outdated stereotypes, technology has made remote work more accessible for older adults than ever before.

What Happened to David and Linda

After our initial call in March, I spent three sessions with David and Linda reviewing their complete financial picture. What we found was both concerning and fixable.

Their withdrawal rate had crept up to 5.1% without them realizing it. Linda’s Part D plan was covering only 60% of a brand-name medication that had a generic equivalent on a competitor plan, costing them an extra $185 a month. Their homeowner’s insurance hadn’t been shopped in four years. And David had been taking his full Social Security benefit since 62, leaving Linda — who earned less during her career — with a spousal benefit that was lower than it needed to be.

We couldn’t undo the early Social Security claim. But we could fix almost everything else. We switched Linda’s Part D plan, saving $2,220 a year. We re-quoted homeowner’s insurance through three carriers and found comparable coverage for $3,800 — saving $1,600 annually. We eliminated $340 in redundant monthly subscriptions. And we restructured their IRA withdrawals to stay below the first IRMAA threshold, which had been costing them an extra $1,680 per year in Medicare surcharges they didn’t even know they were paying.

Total annual savings from these changes: $9,880. Not through dramatic lifestyle cuts. Not through risky investments. Just through paying attention to the details that inflation quietly reshuffled when no one was looking.

“The retirees who weather inflation best aren’t the ones with the biggest portfolios. They’re the ones who review their plan every single year and make adjustments. A retirement plan isn’t a document you create once — it’s a living system that needs annual maintenance, just like your home or your health.”

The Emotional Weight of Financial Anxiety in Retirement

I’d be doing my clients a disservice if I only talked about numbers. The financial stress caused by inflation draining retirement savings takes a real toll on mental health. A 2025 study from the National Council on Aging found that 61% of adults over 65 reported “significant anxiety” about outliving their money — up from 48% in 2021.

David told me something during our second meeting that stuck with me: “I feel like I failed. I did everything right — saved for 40 years, lived below my means, didn’t take on debt. And now I’m watching it disappear.” That sentiment is heartbreakingly common, and it’s almost always misplaced. Retirees didn’t fail. The economic environment shifted in ways that no planning model from 2015 anticipated.

If you or a loved one is feeling this kind of weight, please know that financial stress and emotional well-being are deeply connected. Sometimes the best first step isn’t a spreadsheet — it’s a conversation with someone who understands. Resources like supporting aging parents with depression offer practical guidance that extends beyond finances into the emotional realities of aging.

Looking Ahead: What 2027 Could Bring

There are reasons for cautious optimism. The Social Security Administration is projecting a 2027 COLA that could add approximately $97 per month to the average retiree’s benefit, based on current CPI-W trends. If that holds, it would represent the most meaningful inflation adjustment since the 3.2% increase in 2024.

Additionally, the SECURE 2.0 Act continues to phase in provisions that help older savers. In 2026, catch-up contribution limits for 401(k) participants aged 60–63 increased to $11,250, up from the standard $7,500 catch-up. For late-career savers trying to bolster their retirement cushion, that’s an extra $3,750 per year in tax-advantaged savings — which, in a 22% tax bracket, also reduces your current tax bill by $825.

I’m also watching the IRS closely for potential adjustments to IRMAA thresholds and standard deduction increases for 2027, which could provide additional relief. The additional standard deduction for taxpayers 65 and older is $1,950 for single filers and $1,550 per spouse for married couples in 2026, and these tend to adjust upward with inflation.

The Bottom Line: You’re Not Powerless

Inflation is real, it’s persistent, and it’s draining retirement savings in ways that feel invisible until suddenly they’re not. But the situation is far from hopeless. Every single client I’ve worked with over the past two years — including David and Linda — has found meaningful ways to slow the bleed, restructure their income, and extend their financial runway.

The key is refusing to set your retirement plan on autopilot. Review it annually. Question every premium, every withdrawal, every tax assumption. And if something doesn’t make sense, ask a professional — a CPA, an Enrolled Agent, a fee-only financial planner — before a small oversight becomes a $10,000 annual problem.

David called me again last month. His voice sounded different — lighter. “We’re not out of the woods,” he said, “but for the first time in two years, I feel like we have a path.” For practical next steps that go beyond what we’ve covered here, take a look at six retirement must-knows for 2026 that could save your savings.

That path exists for you, too. You just have to be willing to walk it — one informed decision at a time.

About Robert Thompson, CPA, EA (Enrolled Agent)

Robert Thompson is a Certified Public Accountant and IRS Enrolled Agent with over 20 years of experience specializing in retirement tax planning. He has helped thousands of American retirees navigate the tax implications of Social Security benefits, required minimum distributions, 401(k) and IRA withdrawals, and estate planning. At Daily Trends Now, Robert breaks down complex tax rules into clear, actionable strategies that help seniors keep more of their hard-earned money.