Key Takeaways

- Inflation-adjusted retirement withdrawals are draining portfolios 18-24 months faster than projections from just three years ago.

- The 2026 Social Security COLA of roughly 2.5% may not keep pace with real-world senior spending on healthcare, food, and housing.

- Strategic Roth conversions, Medicare premium optimization, and tax-bracket management can recover thousands of dollars annually.

- Retirees who delay addressing inflation erosion risk running short of funds by their late 70s or early 80s.

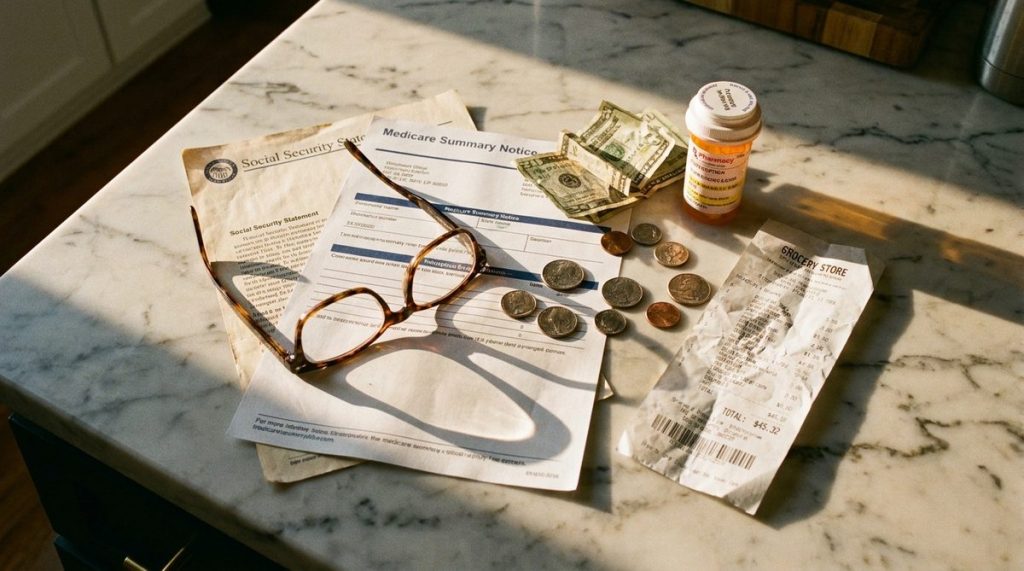

The Silent Threat That’s Accelerating Portfolio Depletion

In my 20 years as a CPA and Enrolled Agent, I’ve watched plenty of economic cycles come and go. But the inflation environment retirees are navigating right now is genuinely different. It’s not a single spike that fades — it’s a persistent, compounding pressure that quietly accelerates how fast retirement savings disappear.

A 2024 survey by the Employee Benefit Research Institute found that 45% of retirees reported spending more than planned, with inflation cited as the primary culprit. By early 2025, the Federal Reserve Bank of New York’s consumer expectations survey showed Americans 60 and older anticipating 3.4% inflation over the next year — well above the Fed’s 2% target.

What I see most often in my practice is this: clients who built their retirement plans around a 2% annual inflation assumption are now watching their money evaporate 18 to 24 months faster than originally projected. That gap may not sound dramatic on paper, but when you’re 74 and staring at a balance that was supposed to last until 90, it’s terrifying.

Here are seven specific, actionable ways inflation is cutting into retirement savings — and what you can do about each one right now.

1. The Social Security COLA Isn’t Keeping Up With Senior-Specific Inflation

The Social Security Administration calculates the annual Cost-of-Living Adjustment (COLA) using the Consumer Price Index for Urban Wage Earners (CPI-W). The problem? That index tracks spending patterns of working-age urban households — not retirees. The 2026 COLA is projected at roughly 2.5%, down significantly from the 3.2% adjustment in 2025 and the 8.7% bump retirees received in 2023.

Meanwhile, the experimental CPI-E (which weights healthcare and housing more heavily to reflect senior spending) consistently runs 0.2 to 0.3 percentage points higher than CPI-W. Over a 20-year retirement, that gap compounds into tens of thousands of lost purchasing power.

I often tell my clients that the COLA is a floor, not a ceiling. If you’re relying on Social Security alone to handle inflation, you’re losing ground every single year. For a deeper look at how the 2026 adjustment specifically affects your benefits, check out this breakdown of Social Security COLA myths that are costing retirees in 2026.

What to do about it

- Build a personal inflation rate based on your actual spending categories — healthcare, property taxes, groceries, and insurance premiums — rather than trusting the national CPI number.

- If you haven’t claimed Social Security yet and can afford to delay, every year you wait past full retirement age adds an 8% permanent increase to your benefit, which compounds on top of future COLAs.

2. Medicare Premiums Are Swallowing Your COLA Increase Before You See It

Here’s the mechanism almost nobody talks about until it hits their bank account: Medicare Part B premiums are deducted directly from your Social Security check. When those premiums rise — and they’ve risen from $148.50/month in 2021 to $185/month in 2025 — they effectively cancel out a significant chunk of your COLA increase.

For 2026, the Medicare Trustees project another increase, potentially pushing Part B premiums above $190/month. If the COLA delivers a $50/month raise but Medicare takes back $30 of it, your net improvement is just $20. That’s before we even talk about Part D prescription drug premiums or Medigap plan increases.

The Income-Related Monthly Adjustment Amount (IRMAA) makes this even worse for retirees with modified adjusted gross incomes above $106,000 (single) or $212,000 (married filing jointly). One-time income events — selling a home, taking a large IRA distribution, realizing capital gains — can push you into a higher IRMAA bracket for the following two years.

I’ve written about this issue extensively, and you can find detailed strategies in this article on how rising Medicare premiums are eating your Social Security check.

What to do about it

- Plan major asset sales or Roth conversions carefully to avoid IRMAA bracket jumps. Two years of surcharges on a $150,000 capital gain can cost an additional $2,000-$5,000 in premiums.

- File an IRMAA appeal (SSA-44 form) if you’ve experienced a qualifying life-changing event — retirement, divorce, death of a spouse — that reduced your income.

3. Grocery and Food Costs Hit Seniors Disproportionately Hard

Between January 2021 and December 2024, cumulative food-at-home prices rose approximately 25%, according to Bureau of Labor Statistics data. While the year-over-year rate has slowed, those elevated prices are now the permanent baseline. Your eggs aren’t going back to $2 a dozen.

Seniors on fixed incomes feel this more acutely because food represents a larger share of their total spending compared to younger households. USDA data shows that adults 65 and older in the lowest income quartile spend roughly 15-17% of their income on food, compared to about 10% for middle-income working-age adults.

What to do about it

- If your income qualifies, the Supplemental Nutrition Assistance Program (SNAP) has specific provisions for households where all members are 60 or older, including higher asset limits.

- Review whether you qualify for the Commodity Supplemental Food Program (CSFP), which provides monthly food packages to low-income seniors. Contact your local Area Agency on Aging for details.

- Factor real grocery inflation — not the headline CPI number — into your annual budget recalculation.

4. The 4% Withdrawal Rule Is Dangerously Outdated in a High-Inflation Environment

The traditional 4% rule — withdraw 4% of your portfolio in year one, then adjust for inflation each subsequent year — was developed by financial planner William Bengen in 1994 using historical data that included lower sustained inflation periods. In my practice, I’ve been telling clients since 2022 that this rule needs serious recalibration.

Research from Investopedia and Morningstar now suggests a more sustainable starting withdrawal rate of 3.3% to 3.7%, depending on your asset allocation and expected retirement length. If you retired in 2021 using 4% and have been adjusting upward for inflation, you’ve likely withdrawn 15-20% more than you originally planned by now.

That’s real money. On a $500,000 portfolio, the difference between a 4% and 3.5% withdrawal rate is $2,500 per year. Over 25 years, with compounding growth, that gap widens to $60,000 or more in preserved capital.

What to do about it

- Adopt a dynamic withdrawal strategy: take less in down-market years, slightly more in strong years, rather than mechanically adjusting for inflation regardless of portfolio performance.

- Establish a two-year cash buffer (in high-yield savings or short-term Treasuries) so you’re never forced to sell equities in a down market to fund living expenses.

5. Property Taxes and Home Insurance Are Rising Faster Than Overall Inflation

Even retirees who own their homes free and clear are seeing carrying costs explode. According to the National Association of Realtors, median property taxes increased 4.1% nationally in 2024, with some Sun Belt states — where many retirees relocate — seeing increases of 6-8%. Homeowners insurance premiums have surged even faster, with the Insurance Information Institute reporting average annual increases of 7-12% since 2022.

For retirees planning to age in place, these costs represent a growing fixed obligation that most retirement calculators underestimate or ignore entirely.

What to do about it

- Check whether your state offers a property tax exemption, freeze, or deferral for seniors. At least 30 states have some form of senior property tax relief, but many require an annual application.

- Shop your homeowners insurance every two to three years. Bundling with auto insurance, raising your deductible to $2,500, and installing storm-resistant features can reduce premiums 15-25%.

- If your home’s assessed value has spiked, consider filing a formal tax assessment appeal. Success rates vary by jurisdiction but often run between 30% and 50%.

6. Healthcare Costs Beyond Medicare Are the Largest Wildcard

Fidelity’s widely cited annual estimate puts the average 65-year-old couple’s lifetime healthcare costs in retirement at $351,000 as of 2024 — and that figure doesn’t include dental, vision, hearing aids, or long-term care. When you add dental and vision expenses (which Original Medicare doesn’t cover), the real number climbs considerably higher.

What concerns me most as a tax professional is that many retirees don’t realize healthcare spending can also trigger cascading tax consequences. Large out-of-pocket medical expenses that exceed 7.5% of your adjusted gross income are deductible — but only if you itemize. Since the 2017 Tax Cuts and Jobs Act nearly doubled the standard deduction ($15,700 for single filers 65+ in 2025), most seniors no longer itemize, which means they lose that deduction entirely.

What to do about it

- If you’re still working at 55 or older and have access to a Health Savings Account (HSA), maximize contributions. HSA funds grow tax-free and can be withdrawn tax-free for qualified medical expenses at any age — making them the single most tax-efficient vehicle for healthcare costs in retirement.

- Consider “bunching” medical expenses into a single tax year to clear the 7.5% AGI threshold and itemize deductions in that year, then take the standard deduction in alternating years.

- Look into Medicare Advantage plans that include dental, vision, and hearing coverage. The trade-off is network restrictions, but for many retirees the out-of-pocket savings are substantial.

7. Tax Bracket Creep Is the Inflation Tax Nobody Warns You About

This is the one I see catch retirees completely off guard. While federal tax brackets do adjust for inflation annually, they adjust based on chained CPI — which historically understates the inflation retirees experience. Meanwhile, several income triggers don’t adjust at all, or adjust slowly:

- The thresholds for Social Security benefit taxation ($25,000 single / $32,000 married filing jointly for up to 50% taxation; $34,000 / $44,000 for up to 85%) haven’t changed since 1993. Inflation has eroded these thresholds so dramatically that roughly 56% of Social Security recipients now owe federal taxes on their benefits, compared to about 10% when the thresholds were set.

- Net Investment Income Tax (NIIT) kicks in at $200,000 for single filers — a threshold set in 2013 with no inflation adjustment.

- The potential 2026 Social Security tax cliff, when provisions of the 2017 tax law are set to expire, could push many retirees into higher effective tax rates.

According to the IRS, the number of tax returns filed by Americans 65 and older showing adjusted gross income between $50,000 and $100,000 has grown 22% since 2019 — not because seniors are earning more in real terms, but because inflation has pushed nominal incomes higher while key thresholds remain frozen.

What to do about it

- Explore strategic Roth conversions during low-income years (the gap between retirement and Required Minimum Distributions starting at age 73). Converting traditional IRA funds to a Roth at today’s tax rates can save tens of thousands if rates rise after 2025.

- Work with a qualified CPA or Enrolled Agent to run multi-year tax projections. A one-year snapshot doesn’t capture how RMDs, Social Security taxation, and IRMAA interact over time.

- Consider qualified charitable distributions (QCDs) from your IRA. If you’re 70½ or older, donating up to $105,000 directly from your IRA to charity satisfies your RMD without increasing your AGI — protecting you from IRMAA surcharges and Social Security taxation simultaneously.

The Bottom Line: Inflation Demands an Active Defense

The hardest thing about inflation cutting into retirement savings is that it doesn’t announce itself. There’s no single catastrophic event — just a steady erosion that shows up as a slightly smaller grocery haul, a slightly larger insurance bill, and a slightly faster decline in your portfolio balance.

In my experience, the retirees who navigate inflation successfully aren’t the ones with the biggest nest eggs. They’re the ones who review their numbers annually, adjust their withdrawal strategy, stay proactive about tax planning, and refuse to assume that last year’s plan still works this year.

If you take one action after reading this article, make it this: sit down this month and calculate your personal inflation rate based on what you actually spend — not what the government says the average American spends. That single exercise has saved my clients more money than almost any other piece of advice I give.

Frequently Asked Questions

How much is the Social Security COLA for 2026?

The 2026 Social Security COLA is projected at approximately 2.5%, based on CPI-W data through the third quarter of 2025. This is a notable decline from the 3.2% COLA in 2025 and the 8.7% adjustment in 2023, meaning retirees will see smaller benefit increases while many real-world costs continue rising.

Is the 4% withdrawal rule still safe for retirees in 2026?

Most financial researchers now recommend a starting withdrawal rate closer to 3.3%-3.7%, especially for retirees expecting a 25-30 year retirement. The traditional 4% rule was based on historical conditions that included lower sustained inflation. A dynamic withdrawal strategy that adjusts based on market performance and actual inflation is generally more sustainable.

How do Medicare premium increases affect my Social Security check?

Medicare Part B premiums are deducted directly from your Social Security payment. When premiums increase — as they have every year recently — they reduce the net amount deposited into your bank account, often absorbing a significant portion of your annual COLA increase. Higher-income retirees face additional IRMAA surcharges that can multiply this effect.

What is the best way to protect retirement savings from inflation?

A multi-pronged approach works best: maintain a diversified portfolio with some inflation-hedging assets (like TIPS and equities), adopt a dynamic withdrawal strategy, maximize tax efficiency through Roth conversions and qualified charitable distributions, build a cash buffer for down markets, and recalculate your personal inflation rate annually based on actual spending.

Will taxes on Social Security benefits change in 2026?

Potentially, yes. The 2017 Tax Cuts and Jobs Act provisions are scheduled to expire at the end of 2025, which could result in higher marginal tax rates for many retirees starting in 2026. Additionally, the income thresholds that trigger taxation of Social Security benefits ($25,000 single / $32,000 married) haven't been adjusted since 1993, meaning inflation continues to push more retirees above these thresholds each year.

About Robert Thompson, CPA, EA (Enrolled Agent)

Robert Thompson is a Certified Public Accountant and IRS Enrolled Agent with over 20 years of experience specializing in retirement tax planning. He has helped thousands of American retirees navigate the tax implications of Social Security benefits, required minimum distributions, 401(k) and IRA withdrawals, and estate planning. At Daily Trends Now, Robert breaks down complex tax rules into clear, actionable strategies that help seniors keep more of their hard-earned money.