The Couple Who Did Everything Right — And Still Worried

When Linda and George Brennan retired in early 2023, they had $1.04 million in combined retirement savings, a paid-off home in suburban Ohio, and two Social Security checks totaling $4,200 a month. By every conventional measure, they’d won the retirement game. George had worked 34 years in manufacturing management. Linda had been a school administrator. They’d saved diligently, avoided debt, and followed the standard playbook.

Then came 2024 and 2025. Grocery bills that once ran $600 a month crept past $800. Their supplemental health insurance premiums jumped 12%. The roof needed replacing — $14,000, not the $9,000 they’d budgeted five years earlier. By the time I spoke with Linda at a financial literacy event in Columbus last fall, she told me something I hear with alarming frequency: “We have a million dollars and we’re scared to spend it.”

The Brennans aren’t alone. According to a 2025 Employee Benefit Research Institute survey, 48% of retirees with assets between $500,000 and $1.5 million say they feel “not confident” or only “somewhat confident” their money will last. And that anxiety isn’t irrational — it’s a rational response to a financial landscape that has shifted beneath their feet.

So can you retire on $1 million in 2026? The honest answer, after 15 years analyzing consumer finance data, is: it depends entirely on where you live, how you plan, and whether you’re willing to make a few strategic moves that most retirees overlook.

The Million-Dollar Myth: What $1 Million Actually Buys Now

A million dollars sounds like a fortress of security. But in 2026, that fortress has thinner walls than most people realize. Let’s start with the math that matters.

The traditional “4% rule” — withdraw 4% of your portfolio annually, adjusted for inflation — suggests a $1 million nest egg can safely produce $40,000 per year. That was designed by financial planner William Bengen in 1994, based on historical market returns and a 30-year retirement horizon. It remains a useful starting point, but in my experience, it’s often misapplied.

Here’s why: the 4% rule assumes a balanced stock-and-bond portfolio. But many retirees I’ve worked with have shifted heavily into bonds or cash equivalents out of fear — especially after the 2022 market downturn. A portfolio yielding 3% instead of the blended 7% the rule assumes means your money works significantly less hard. That $40,000 annual withdrawal could start depleting principal much faster than expected.

Geography Is Destiny

Where you retire on $1 million matters as much as how much you have. The Bureau of Economic Analysis data on regional price parities shows dramatic variation across the United States:

- In Mississippi, Arkansas, or West Virginia, $1 million plus average Social Security benefits can support a comfortable 25- to 30-year retirement.

- In Ohio, Missouri, or Tennessee, it stretches well — but requires discipline and a real budget.

- In California, Massachusetts, New York, or Hawaii, $1 million alone is unlikely to sustain a 25-year retirement without significant supplemental income.

A 2026 analysis by Investopedia found that a retiree spending $65,000 annually — a realistic figure that includes housing, healthcare, food, and modest leisure — would exhaust $1 million in roughly 18 years in a mid-cost state, assuming a conservative 4.5% average annual return. In a high-cost state, that window shrinks to 13-14 years.

The Inflation Factor Seniors Can’t Ignore in 2026

Inflation is the silent partner at every retiree’s table. While the Consumer Price Index has moderated from its 2022 peak of 9.1%, the CPI-E — the experimental index that tracks spending patterns of Americans 62 and older — consistently runs higher than the headline number. Why? Because seniors spend disproportionately more on healthcare and housing, two categories where prices have remained stubbornly elevated.

In 2025, medical care services rose 3.8% year-over-year, and shelter costs climbed 4.2%. For a retiree on a fixed income, these aren’t abstract percentages — they’re the difference between refilling a prescription or skipping it, between maintaining the house or letting repairs slide.

What I see most often is a dangerous psychological pattern: retirees cut spending on things that seem optional — preventive healthcare, home maintenance, social activities — which then creates larger, more expensive problems down the line. A $200 gutter cleaning skipped today becomes a $6,000 water damage repair next year. If you’re weighing those kinds of decisions, our guide on inflation draining retirement savings and seven moves seniors must make now lays out practical defensive strategies.

The Healthcare Cost Nobody Budgets For

Fidelity’s 2025 Retiree Health Care Cost Estimate puts the average 65-year-old couple’s lifetime healthcare spending at $351,000 — and that assumes they have Medicare. Out-of-pocket costs for dental, vision, hearing, and long-term care can easily push that figure past $400,000.

When you subtract that from a $1 million nest egg, you’re really working with $600,000 to $650,000 for everything else over a 20- to 30-year retirement. That reframes the question entirely.

Social Security: Your Most Underrated Asset

Here’s something I often tell readers that surprises them: for most American retirees, Social Security is worth more than their savings. The average retired worker’s benefit in 2026 is approximately $1,976 per month, or $23,712 per year. Over a 20-year retirement, that’s $474,240 — and it’s inflation-adjusted annually through the cost-of-living adjustment (COLA).

If you can delay claiming until age 70, your benefit grows by approximately 8% per year beyond full retirement age. For someone with a full retirement age benefit of $2,200, waiting until 70 boosts that to roughly $2,900. Over 20 years of collecting, that delay generates an additional $168,000 in lifetime benefits — guaranteed, inflation-adjusted income that no market downturn can touch.

The Social Security Administration provides free benefit calculators that let you model different claiming ages. I recommend every person within five years of retirement run these numbers at least annually. And if you’re already collecting, learning how to stretch your Social Security check in 2026 can make a meaningful difference in your monthly cash flow.

The Spousal Strategy Most Couples Miss

Married couples have a significant advantage that’s frequently underutilized. The higher earner can delay benefits to 70 while the lower earner claims at full retirement age (or even 62, depending on the situation). This provides household income while the larger benefit grows. When the higher earner passes away, the surviving spouse receives the larger of the two benefits — creating a form of longevity insurance that’s built right into the system.

In my 15 years of experience analyzing consumer finance outcomes, coordinated spousal claiming strategies are one of the highest-impact, lowest-cost financial moves available to retirees. Yet fewer than 30% of couples I’ve encountered have actually modeled this.

Making $1 Million Last: The Real Playbook

Theory is useful. Strategy is better. Here’s what actually works for retirees who need to make $1 million stretch across decades — not based on hypothetical models, but on patterns I’ve observed across thousands of consumer finance cases.

Build a Spending Floor Before a Spending Ceiling

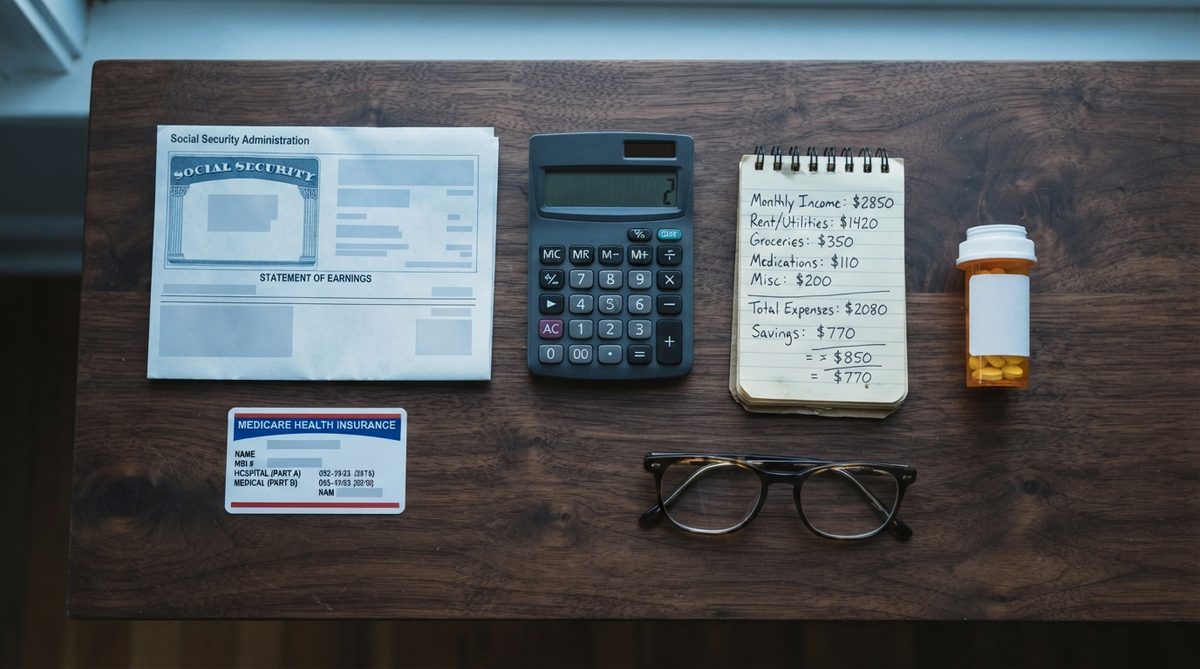

Before calculating how much you can spend, determine how much you absolutely must spend. This is your non-negotiable floor: housing costs, Medicare premiums and out-of-pocket health expenses, food, utilities, insurance, and transportation. For most retirees, this floor lands between $2,800 and $4,500 per month, depending on whether the home is paid off and which state they live in.

If Social Security covers your spending floor — or comes close — your $1 million becomes a supplement for quality of life, emergencies, and legacy, rather than a lifeline you’re terrified of draining. That psychological shift is enormous.

Use a Bucket Strategy, Not a Single Pot

One approach that has proven effective for retirees managing anxiety and market risk is the “bucket” system:

- Bucket 1 (Years 1-3): Cash and short-term instruments — enough to cover 2-3 years of withdrawals. This prevents forced selling during a downturn.

- Bucket 2 (Years 4-10): Bonds, dividend-paying stocks, and balanced funds. Moderate growth with moderate risk.

- Bucket 3 (Years 10+): Growth-oriented investments. With a decade-plus time horizon, this money can weather volatility and benefit from compounding.

This structure lets retirees ride out bear markets without panic selling — which, according to CFPB research, is one of the top three financial mistakes Americans over 62 make.

Right-Size Your Housing — But Do It Strategically

Housing is typically a retiree’s largest expense. If you own your home outright, you’ve already removed the single biggest drain on retirement savings. But maintenance, property taxes, insurance, and utilities still add up — often $800 to $1,500 per month even without a mortgage.

Downsizing can free up significant capital. A couple selling a $350,000 home and purchasing a $200,000 condo or smaller property unlocks $150,000 (minus transaction costs) that can be added to their investment portfolio or used to fund several years of living expenses. Others are choosing to stay put and modify their current home — if you’re considering that route, there’s an excellent breakdown of how to set up your home to age in place for under $1,500 that covers high-impact, low-cost modifications.

The Tax Landmines Hiding in Your Retirement Accounts

Here’s a detail that catches many retirees off guard: not all of that $1 million is yours. If the bulk of your savings sits in traditional 401(k) or IRA accounts, every dollar you withdraw is taxed as ordinary income. Depending on your tax bracket and state taxes, you could owe 12% to 22% — or more — on each withdrawal.

A million dollars in a traditional IRA is really $780,000 to $880,000 after taxes. A million dollars in a Roth IRA, by contrast, is a full million — because qualified withdrawals are tax-free.

For those still in the planning phase, strategic Roth conversions during lower-income years (say, between retirement at 62 and Social Security claiming at 67 or 70) can dramatically reduce your lifetime tax burden. The IRS provides detailed guidance on conversion rules and income thresholds. Even partial conversions of $20,000 to $50,000 per year can shift tens of thousands of dollars from taxable to tax-free status over a decade.

Required Minimum Distributions: The Forced Withdrawal Problem

Starting at age 73 (under the SECURE 2.0 Act), the IRS requires you to begin withdrawing from traditional retirement accounts whether you need the money or not. These required minimum distributions (RMDs) can push you into a higher tax bracket, increase your Medicare premiums through IRMAA surcharges, and even make more of your Social Security benefits taxable.

I’ve seen retirees blindsided by an unexpected $3,000 to $5,000 annual increase in Medicare premiums simply because their RMDs pushed their modified adjusted gross income above the IRMAA threshold. Planning for this in advance — not after it happens — is critical.

The Emotional Side of Spending Down a Nest Egg

Numbers matter. But after analyzing thousands of retirement cases, I can tell you that the psychological dimension of retirement spending is just as important as the math — and far less discussed.

Many retirees with $1 million or more suffer from what researchers at the MIT AgeLab call “spending paralysis.” They’ve spent 30 or 40 years accumulating wealth, and the mental shift to decumulation — actually spending their savings — feels terrifying. The result? They live far below their means, denying themselves experiences, healthcare, and comfort they can genuinely afford.

Linda Brennan told me she felt guilty buying a $45 sweater. Her husband hadn’t seen a dentist in two years because the $300 out-of-pocket cost “felt like too much.” They have over $900,000 in savings. This is not a financial problem. It’s a psychological one — and it’s remarkably common.

If this resonates with you, I’d encourage working with a fee-only financial planner (not one who earns commissions on products) who can build a withdrawal plan that gives you explicit permission to spend. Sometimes seeing the math laid out by a professional is what it takes to exhale.

The Bottom Line: $1 Million Is Enough — With a Plan

Can you retire on $1 million in 2026? Yes — but only if you treat it as a resource to be managed, not a magic number that guarantees security on its own. The retirees who thrive with $1 million share a few common traits: they know their actual spending floor, they’ve coordinated Social Security timing, they’ve addressed tax efficiency, and they’ve made intentional housing decisions.

The retirees who struggle — even with $1 million or more — are typically those who never built a drawdown plan, who let fear drive investment decisions, or who ignored healthcare cost planning until bills arrived.

George and Linda Brennan are going to be fine. After our conversation, they connected with a fee-only advisor, restructured their withdrawal strategy, and George finally went to the dentist. Linda bought the sweater. They still have over $900,000, a paid-off home, and two Social Security checks that cover their essential expenses.

A million dollars isn’t what it was in 1995. But managed wisely, it’s still a foundation that can support a dignified, comfortable, even joyful retirement. The key is refusing to let fear replace planning — and starting that planning today, whether you’re 52 or 72.

Frequently Asked Questions

Can you retire on $1 million in a high-cost state like California or New York?

It's significantly harder. In high-cost states, a $1 million nest egg plus average Social Security may only sustain 13-15 years of retirement spending. Retirees in these areas often need to supplement with part-time income, downsize aggressively, or consider relocating to a lower-cost region to make the math work over a 25- to 30-year retirement.

How much should a retiree withdraw from savings each year to avoid running out of money?

The traditional guideline is 4% of your portfolio in the first year, adjusted for inflation thereafter. However, many financial planners now recommend a more flexible approach — withdrawing 3.5% to 4.5% depending on market conditions and personal spending needs. In years when markets decline significantly, reducing withdrawals temporarily can extend the life of your savings by several years.

Does the $1 million retirement figure include expected healthcare costs?

It should, but many retirees fail to account for healthcare separately. Fidelity estimates the average 65-year-old couple will spend $351,000 on healthcare in retirement, even with Medicare. Subtracting that from $1 million leaves roughly $650,000 for all other expenses, which is why healthcare planning is a critical part of retirement budgeting.

At what age should I claim Social Security to make $1 million last longer?

Delaying Social Security until age 70 — if your health and finances allow it — maximizes your guaranteed monthly income by roughly 8% per year past full retirement age. This higher, inflation-adjusted income reduces the amount you need to withdraw from savings, effectively extending how long your $1 million lasts.

Should I convert my traditional IRA to a Roth IRA before retirement?

Strategic partial Roth conversions during lower-income years can significantly reduce your lifetime tax burden and protect you from higher taxes on required minimum distributions later. However, conversions trigger taxable income in the year they occur, so it's important to work with a tax professional to determine the right conversion amounts and timing for your specific situation.

About Sarah Mitchell, Former CFPB Senior Analyst

Sarah Mitchell is a consumer finance expert with 15 years of experience protecting American consumers. She spent eight years as a senior analyst at the Consumer Financial Protection Bureau (CFPB), where she investigated financial fraud targeting older adults and developed consumer education programs. At Daily Trends Now, Sarah covers scam awareness, smart shopping strategies, discount programs, and consumer rights — helping seniors protect their wallets and avoid costly traps.